InstitutionsBlogCompany

Alpha Report October Recap

November 15, 2024

Key Takeaways

*All data is as of October 31st, 2024

Market Performance

As of October 31st, 2024, the Standard and Poor’s 500 (“S&p 500”) fell 0.99% in the past month and has risen +25% on an annual basis, respectively. Bitcoin (“BTC”) rose 15.63% and +136.6% in the past month and on an annual basis, respectively. The recent upturn is primarily attributed to the latest and projected interest rate cuts by central banks, both domestically and internationally.

The U.S. Treasury 10-year rate fell 9.3 basis points over the past month. October yielded a -0.74% monthly loss in the US Dollar. Dow Jones, U.S. High-Yield, U.S. Investment Grade, and gold changed by +1.85%, +1.56%%, +1.7%, and 5.34% over the last month, respectively.

As of October 31st, 2024, Bitcoin (“BTC) and Ethereum (“ETH”) gained 15.63% and 2.78% on a monthly basis, respectively. These returns are reflected in our Risk-Adjusted Portfolios (“RAP”) given their dominance in the marketplace. Sentiment and performance in the digital asset market (as proxied by BTC and ETH) has shifted from neutral to bullish recently, driven by an increase in global liquidity stemming from numerous interest rate cuts by major central banks and the election of Donald Trump. Projections indicate that more cuts are likely to close out 2024 and early 2025.

The macro backdrop has strengthened in our Investment Team’s purview. We still believe the next 3-9 months to be constructive for risky assets (see ‘Outlook’ below). While two concurrent geopolitical conflicts remain a risk to the global economy and financial markets, effects appear to be currently limited to specific locales and assets. The primary near-term catalysts appear to be the continued success and proliferation of spot ETFs, domestic and abroad, increasing global liquidity, cyclicality of crypto markets in accordance with Halving cycles, and a political shift in the U.S. that supports cryptocurrency.. The Team remains mid-long term constructive on BTC and the digital asset market as a whole in 2024 and the beginning of 2025.

Portfolio Performance

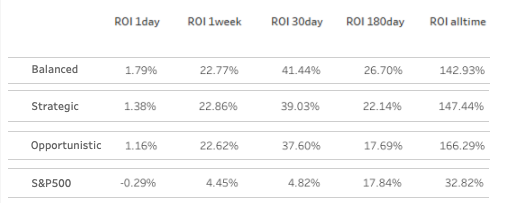

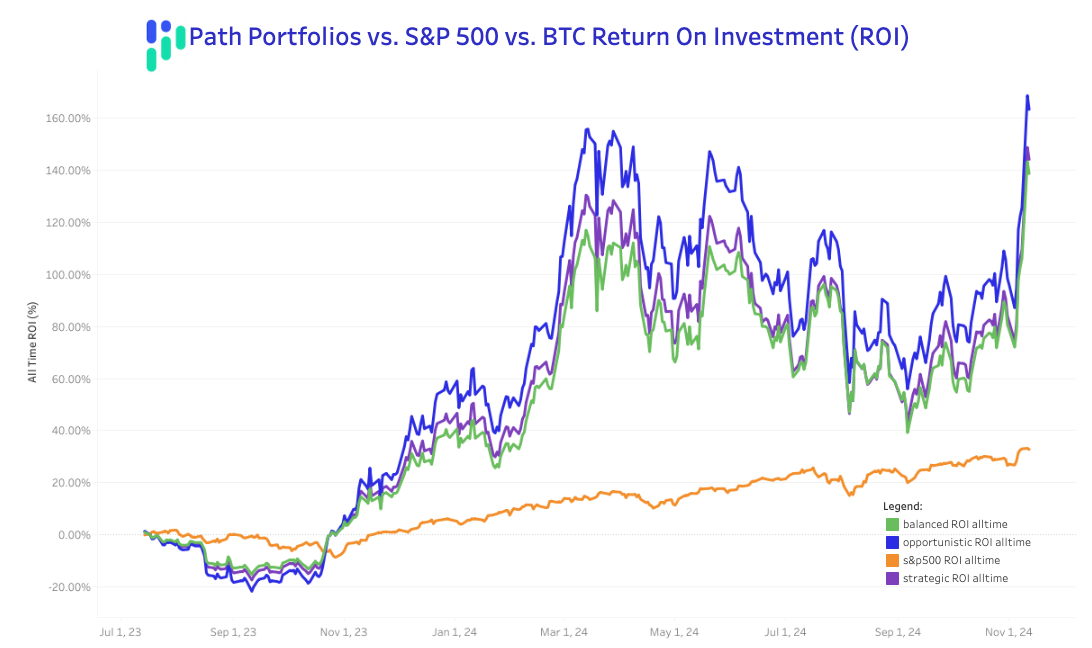

Cumulative returns across the three RAP (Balanced, Strategic, and Opportunistic) portfolios ranged from +80.64% to +98.4% for the period starting July 18th, 2023 through October 31st, 2024. This compares to a +29.46% return in the Standard and Poor’s 500 index (S&P500) over the same period (data below is as of November 14th, 2024).

Cumulative returns across the three RAP (Balanced, Strategic, and Opportunistic) portfolios ranged from +9.84% to +13.68% for the period starting October 1st, 2024 through October 31st, 2024. This compares to a -0.06% return in the Standard and Poor’s 500 index (S&P500) over the same period (data below is as of November 14th, 2024).

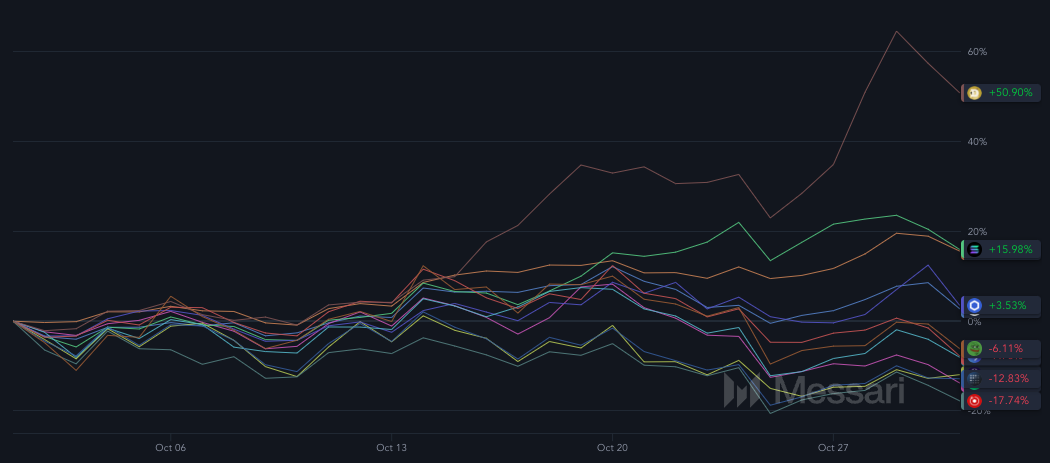

In the two images below, you will find the performance of all assets in Path’s RAP portfolios over the course of October 2024.

The main driver of recent RAP performance is attributed to the Investment Director’s discretionary views to remain fully allocated to risk-on assets for at least the remainder of 2024 and the early part of 2025.

Although crypto markets experienced a stagnant summer trading period, historically dips are common around the Bitcoin halving and the most profitable periods of prior crypto cycles occurred 12-18 months after the halving. We are currently ~6 months post halving.

Outlook

The coordinated actions of major central banks worldwide highlight their commitment to stimulating the economy through quantitative easing. Our Investment Team believes that this approach will enhance global liquidity, which has historically been linked to growth in risk-on sectors, such as digital assets.

Donald Trump’s administration has consistently expressed a willingness to collaborate with the cryptocurrency community in the United States, aiming to promote growth and establish regulations that do not stifle the ecosystem. His upcoming four-year term as president should provide cryptocurrency ample opportunity to further legitimize itself.

In October, cryptocurrencies responded favorably to the adjustments made by the central banks mentioned earlier. Our team anticipates additional rate cuts extending through Q4 2024 and into 2025, which should provide the necessary liquidity to propel digital assets to new heights over the next 3 to 9 months, coinciding with historical halving events.